Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

A form of equity remuneration (non-cash)

Stock Based Compensation (also called Share-Based Compensation or Equity Compensation) is a way of paying employees, executives, and directors of a company with equity in the business. It is typically used to motivate employees beyond their regular cash-based compensation (salary and bonus) and to align their interests with those of the company’s shareholders. Shares issued to employees are usually subject to a vesting period before they are earned and can be sold.

Compensation that’s based on the equity of a business can take several forms.

Common types of compensation include:

Companies compensate their employees by issuing them stock options or restricted shares. The shares typically vest over a few years, meaning, they are not earned by the employee until a specified period of time has passed. If the employee quits the company before the shares have vested, they forfeit those shares. As long as the employee stays long enough with the company, all of their shares will vest. They can hold the shares indefinitely, or sell them to convert them into cash.

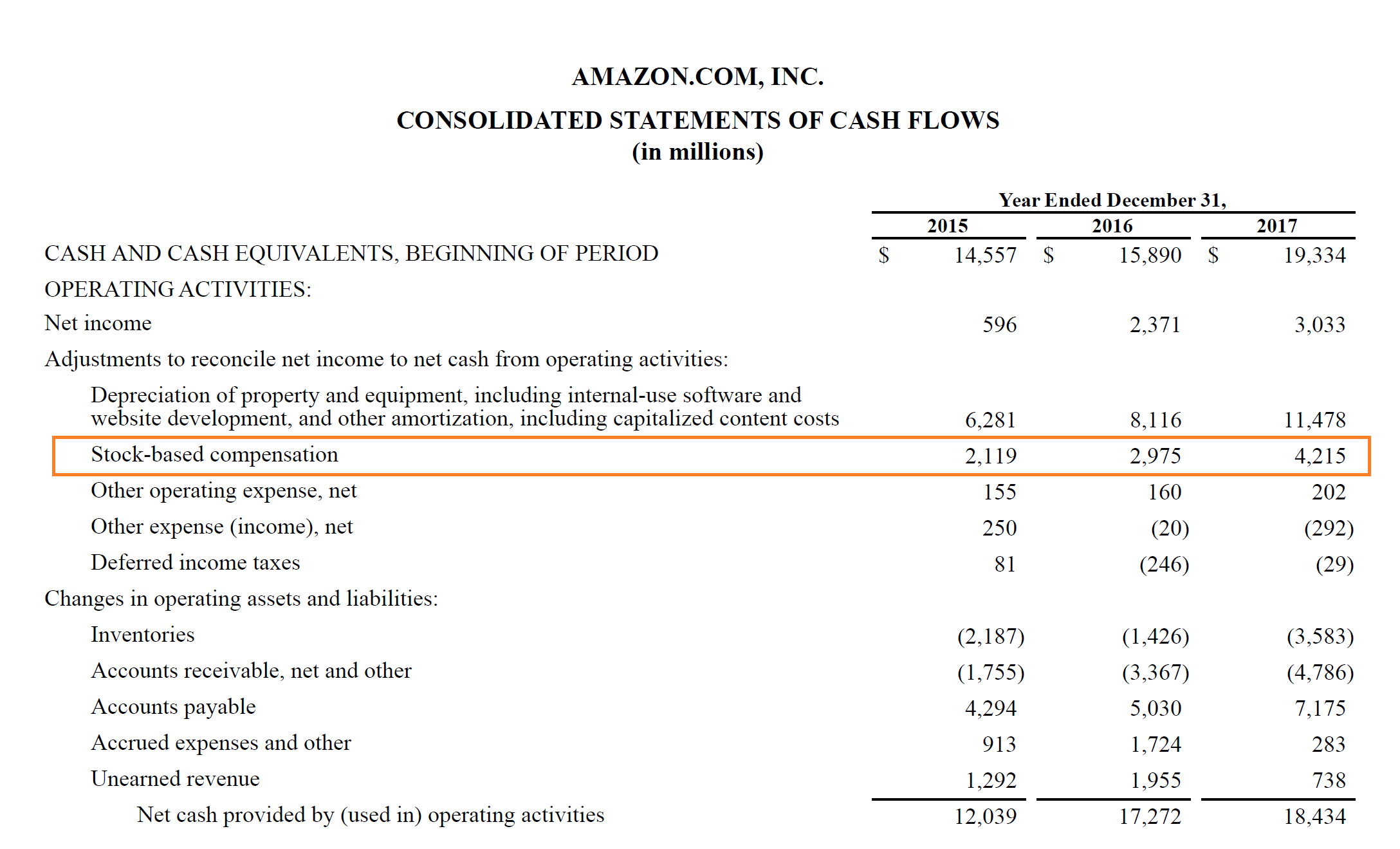

The easiest way to understand how it works is with an example. Let’s look at Amazon’s 2017 annual report and examine how much they paid out in equity to employees, directors, and executives, as well as how they accounted for it on their financial statements.

As you can see in the cash flow statement below, net income must be adjusted by adding back all non-cash items, including stock-based compensation, to arrive at cash from operating activities.

In 2017, Amazon paid $4.2 billion of share-based compensation to its employees.

Since the company has approximately 560,000 employees, that works out to about $7,500 per employee on average.

There are many advantages to this type of remuneration, including:

Challenges and issues with equity remuneration include:

When building a discounted cash flow (DCF) model to value a business, it’s important to factor in share compensation. As you saw in the example from Amazon above, the expense is added back to arrive at cash flow, since it’s a non-cash expense.

While the expense does not require any cash, it does have a capital structure impact on the business, since the number of shares outstanding increases.

Analysts need to decide how to address this issue, and there are two common solutions:

Thank you for reading CFI’s guide to Stock Based Compensation. To continue learning and advancing your career, these CFI resources will be helpful:

Access and download collection of free Templates to help power your productivity and performance.

Already have an account? Log in

Take your learning and productivity to the next level with our Premium Templates.

Upgrading to a paid membership gives you access to our extensive collection of plug-and-play Templates designed to power your performance—as well as CFI's full course catalog and accredited Certification Programs.

Already have a Self-Study or Full-Immersion membership? Log in

Gain unlimited access to more than 250 productivity Templates, CFI's full course catalog and accredited Certification Programs, hundreds of resources, expert reviews and support, the chance to work with real-world finance and research tools, and more.

Already have a Full-Immersion membership? Log in